Black-Scholes-Merton (or BSM) model is the most popular and widely-used option pricing model. Below, there is an example of the calculation of the BSM option price and option Greeks in Excel.

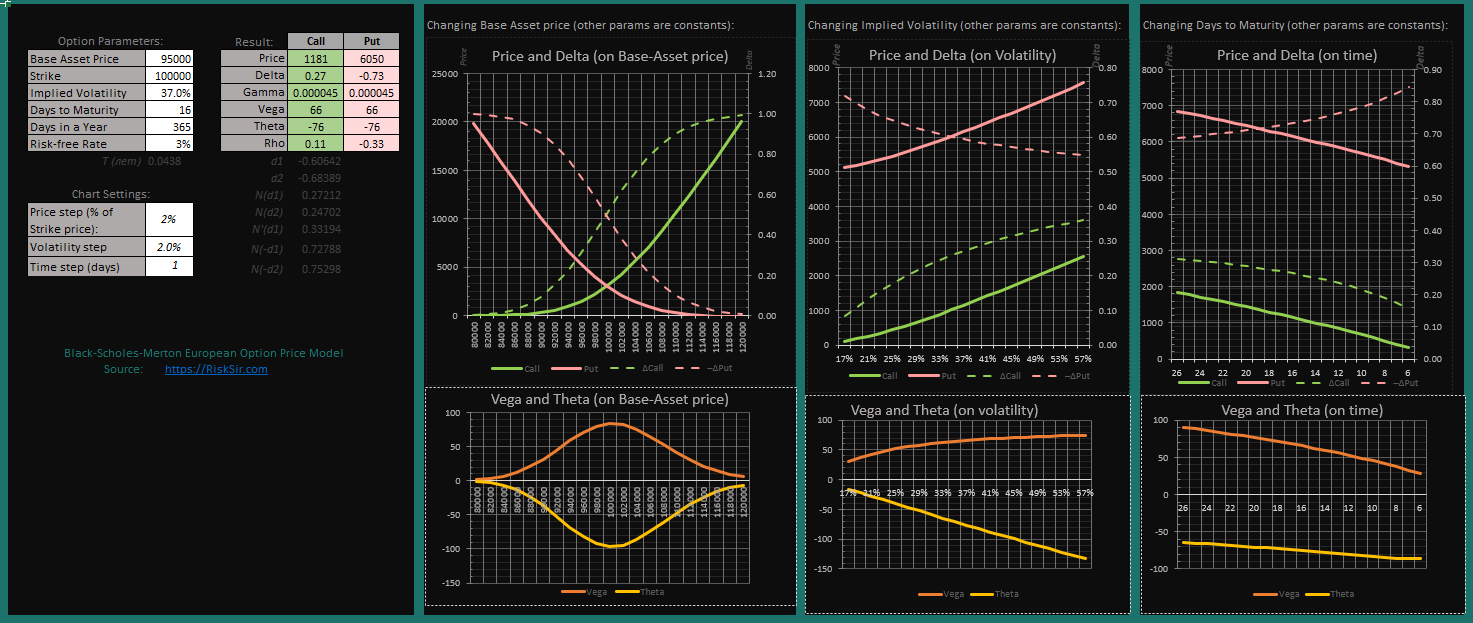

1. Black-Scholes Option Price in Excel without VBA

2. Black-Scholes Option Price in Excel with VBA

'-------------------------------------------------------------------------

' Source: risksir.com

' Description: Black-Scholes-Merton European Option Price Model

'-------------------------------------------------------------------------

'-------------------------------------------------------------------------

' S — Base Asset Price

' X — Strike

' d — Days to maturity (if 0 -> takes 0.3 days)

' y — Days in one year

' v — Implied volatility (if 0 -> takes 10^(-10))

' r — Risk-free rate

'-------------------------------------------------------------------------

' PRICE

Function OptionPrice(OptionType, S, X, d, y, v, r)

If d > 0 Then

T = d / y

Else: T = 0.3 / y

End If

If (OptionType = "Call" Or OptionType = "CALL") Then

OptionPrice = S * Nd_1(S, X, d, y, v, r) - X * Nd_2(S, X, d, y, v, r) * Exp(-r * T)

ElseIf (OptionType = "Put" Or OptionType = "PUT") Then

OptionPrice = X * N_d_2(S, X, d, y, v, r) * Exp(-r * T) - S * N_d_1(S, X, d, y, v, r)

ElseIf (OptionType = "BA") Then

OptionPrice = S

End If

End Function

' DELTA

Function OptionDelta(OptionType, S, X, d, y, v, r)

If (OptionType = "Call" Or OptionType = "CALL") Then

OptionDelta = Nd_1(S, X, d, y, v, r)

ElseIf (OptionType = "Put" Or OptionType = "PUT") Then

OptionDelta = Nd_1(S, X, d, y, v, r) - 1

End If

End Function

' THETA

Function OptionTheta(S, X, d, y, v, r)

If d > 0 Then

T = d / y

Else: T = 0.3 / y

End If

If v = 0 Then v = 10 ^ (-10)

OptionTheta = -((S * v * N1d_1(S, X, d, y, v, r)) / (2 * (T ^ 0.5))) / y

End Function

' GAMMA

Function OptionGamma(S, X, d, y, v, r)

If d > 0 Then

T = d / y

Else: T = 0.3 / y

End If

If v = 0 Then v = 10 ^ (-10)

OptionGamma = N1d_1(S, X, d, y, v, r) / (S * (v * (T ^ 0.5)))

End Function

' VEGA

Function OptionVega(S, X, d, y, v, r)

If d > 0 Then

T = d / y

Else: T = 0.3 / y

End If

If v = 0 Then v = 10 ^ (-10)

OptionVega = (S * (T ^ 0.5) * N1d_1(S, X, d, y, v, r)) / 100

End Function

' RHO

Function OptionRho(S, X, d, y, v, r)

If d > 0 Then

T = d / y

Else: T = 0.3 / y

End If

If v = 0 Then v = 10 ^ (-10)

OptionRho = X * T * Exp(-r * T) * Nd_2(S, X, d, y, v, r) / 10000

End Function

Function d_1(S, X, d, y, v, r)

If d > 0 Then

T = d / y

Else: T = 0.3 / y

End If

If v = 0 Then v = 10 ^ (-10)

d_1 = (Log(S / X) + (r + 0.5 * (v ^ 2)) * T) / (v * (T ^ 0.5))

End Function

Function d_2(S, X, d, y, v, r)

If d > 0 Then

T = d / y

Else: T = 0.3 / y

End If

d_2 = d_1(S, X, d, y, v, r) - v * (T ^ 0.5)

End Function

Function Nd_1(S, X, d, y, v, r)

Nd_1 = Application.NormSDist(d_1(S, X, d, y, v, r))

End Function

Function Nd_2(S, X, d, y, v, r)

Nd_2 = Application.NormSDist(d_2(S, X, d, y, v, r))

End Function

Function N_d_1(S, X, d, y, v, r)

N_d_1 = Application.NormSDist(-d_1(S, X, d, y, v, r))

End Function

Function N_d_2(S, X, d, y, v, r)

N_d_2 = Application.NormSDist(-d_2(S, X, d, y, v, r))

End Function

Function N1d_1(S, X, d, y, v, r)

If d > 0 Then

T = d / y

Else: T = 0.3 / y

End If

N1d_1 = 1 / (2 * Application.Pi()) ^ 0.5 * (Exp(-0.5 * d_1(S, X, d, y, v, r) ^ 2))

End Function